- Purchases within the Home & Garden category spike during lockdown and continue to rise week-on-week across all age demographics

- Health & Beauty spending peaks during the first and second weeks of lockdown but level out as Brits get used to working from home

- Share of spending on Clothing & Shoes rises rapidly in the second week of March as lockdown became a possibility, but decreases as social distancing restrictions come in

London, 8th May 2020 – Klarna, the leading global payments and shopping provider, today released new data that tracks how UK consumer purchasing habits have evolved while under lockdown and as the COVID-19 outbreak continues.

The company, which is used by over 7 million shoppers and has over 5,000 retail partners in the UK, analysed all the transactions made through its retail partners to identify what product categories Gen Zers, Millennials, Gen Xers and Baby Boomers are shopping for most often using Klarna’s flexible payment options.

Klarna analysed purchases by shoppers in the Gen Z (ages 18–23), Millennial (ages 24–39), Gen X (ages 40–55) and Baby Boomer (55+) demographics over the individual weeks from March 9th onwards, as well as comparing overall spending across a base period from 23rd February to 23rd March (the month prior to lockdown), and 23rd March to 23rd April (the first month of lockdown). Klarna separated purchases into seven major categories and then analysed how each category’s share of all Klarna purchases has shifted on a week by week basis within each age group. Over the coming weeks, Klarna will continue to analyse consumer spending data to identify how the coronavirus outbreak is affecting e-commerce and consumer shopping behaviour.

KEY FINDINGS

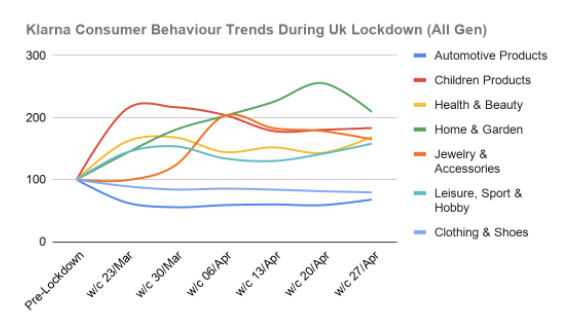

Trends over time

Comparing spending trends for the month prior to lockdown to the month since lockdown, Klarna found that British spending patterns have evolved significantly. The proportion of spending on Home & Garden, Health & Beauty, Leisure, Sport & Hobbies and Children’s Products have all risen. However, Klarna’s data analysis goes further and looks at how the relative share of spending within these categories has evolved on a week by week basis. Key swings occurred in the following categories:

* Index (100) represents each category’s share of the consumer’s wallet before the lockdown. The changes reflect consumers’ share of spending in each category compared to the other categories during the subsequent weeks.

- Home & Garden – Share of purchases within the Home & Garden category spiked from the week before lockdown (beginning 16th Mar) and continued to trend upward week-on-week, perhaps due to an exceptionally good spell of weather and as Brits look to keep themselves busy at home. The last week in April showed a decline, which may well be attributable to the onset of April showers and changeable weather experienced.

- Health & Beauty – As a relative share of total purchases, spending on Health & Beauty products rose rapidly as lockdown became a possibility, seeing an increase of 14% between the week beginning 16th March and 23rd March. However, after an initial rapid increase, spending within this category slowed, perhaps as a reflection of Brits socialising less and as such spending less time (and money) on beauty products. However, the last week of April saw an increase in relative share of purchase of 17%, almost exactly equal to the decrease seen in Home & Garden as Brits retreated indoors.

- Leisure, Sport & Hobbies – Purchases in the Leisure, Sport & Hobbies category also trended upwards as lockdown became a possibility, rising week on week until a week into lockdown itself (30th March) and then fluctuated as customers were faced with spending a greater period of time at home.

- Clothing & Shoes – Spending on Clothing & Shoes spiked in early March, increasing relative share of purchase by 8% between week commencing 2nd of March – 9th March as Brits got their fashion fix ahead of lockdown. Since then, the percentage of overall spending on fashion has decreased rapidly, dropping 15% between the week commencing 9th March – 16th March, the week before social distancing measures fully came into place.

Generational differences

Klarna’s data also broke down spending by age groups, showing how spending patterns have shifted between different generations.

- Gen Z – While Gen Z spend has been moving away from Clothing & Shoes it has done so at a slower rate than other age groups. Share of spending increased the most overall in the Home and Garden category, increasing its relative share by 262% . Whilst the Health & Beauty sector also saw an increase in relative share of 81% between 9th March and 20th April. Laterly (in the last two weeks of Apr) Gen Z’ers have increased their relative share of purchase by 17% on Leisure, Sport & Hobby as they keep themselves entertained at home.

- Millennials – Millennial share of spend in the Leisure, Sport & Hobby category increased by 68% in the two weeks leading up to lockdown (w/c 9th-23rd Mar). Whilst week on week spending saw a particularly large shift towards the Home & Garden category as spending on Clothes & Shoes decreased comparatively. The Home & Garden category specifically saw an increase of 231% of its relative share (w/c 9th Mar – 20th Apr).

- Gen X – Gen X share of spend in the Leisure, Sport and Hobby category saw an increase of 62% in the two weeks leading up lock down (w/c 9th-23rd Mar). Whilst the relative share of spend in the Home & Garden category increased 156 % between week commencing 9th March and 20th April.

- Baby Boomer – Baby Boomer spending dropped the most significantly in the Clothing & Shoes category, decreasing 30% as a relative share between week commencing 9th March and 20th April, whilst in the same period relative spend in the Home & Garden category increased 136%, again consistent with the overarching trend, with the relative share decreasing in the last week of April.

Luke Griffiths, General Manager at Klarna UK, commented: “Our week-by-week breakdown gives an unparalleled look into the shifting mindsets of consumers across the UK. It’s amazing to see how e-commerce purchasing habits have evolved significantly during the period of just a few short weeks. For retailers and brands, the data may indicate an early emphasis on Leisure, Sport & Hobbies and Health & Beauty as consumers chose to buy comfort items to work from home in, as well as workout wear to keep them fit and exercising in their living rooms. The trend skews clearly towards consumers adapting to a longer period of lockdown and life at home in the summer, with the focus moving towards kitting out homes and gardens. Whilst the last week in April and the spell of wet weather saw further indoor activities being explored. Consumers are also taking advantage of flexible online payment options that offer greater control and can help them through this ‘stay-at-home’ period.”

***

Press enquiries:

MHP Communications

+44 (0)20 3128 8100

klarna@mhpc.com

Notes to editors

Methodology:

Klarna analysed UK purchase volumes for items bought through Klarna’s onboarded merchant partners over the individual weeks from March 9th onwards (ending w/c 27th April) as well as comparing overall spending across a base period from 23rd February to 23rd March, and 23rd March to 23rd April. The data were distributed as share of total, and did not account for any increases or decreases of volume within any of the age groups analysed – Gen Z (ages 18–23), Millennial (ages 24–39), Gen X (ages 40–55) and Baby Boomer (55+). The data indicates only the distribution of purchase volumes among the following categories for each age group:

- Clothing & Shoes – Adult/General/Youthful shoes and clothing

- Leisure, Sport & Hobby – Sports and outdoor gear, concept stores, hobby articles, prints and photos, costumes, and party supplies

- Jewellery and Accessories – Including watches, sunglasses, bags and wallets

- Home & Garden – Furniture, tools and home improvement, pet supplies, kitchenware, plants and flowers, cleaning and sanitary products

- Health & Beauty – Cosmetics, fragrances, hair and makeup products, pharmaceuticals, dietary supplements and personal care and body improvement products

- Children’s Products – Diversified children’s products ranging from cots, clothing, nurturing and toys

- Automotive Products – Automotive parts and accessories, wheels, tyres and vehicle servicing

About Klarna

We make shopping smoooth. With Klarna consumers can buy now and pay later, so they can get what they need today. Klarna’s offering to consumers and retailers include payments, social shopping, and personal finances. Klarna has enabled over 85 million consumers to pay with ease and convenience. Over 200,000 merchants, including H&M, IKEA, Expedia Group, Samsung, ASOS, Peloton, Abercrombie & Fitch, Nike and AliExpress have enabled Klarna’s innovative shopping experience online and in-store. Klarna is the most highly valued fintech in Europe with a valuation of $5.5bn and one of the largest private fintechs globally. Klarna was founded in 2005, has over 3,000 employees and is active in 17 countries. For more information, visit klarna.com.