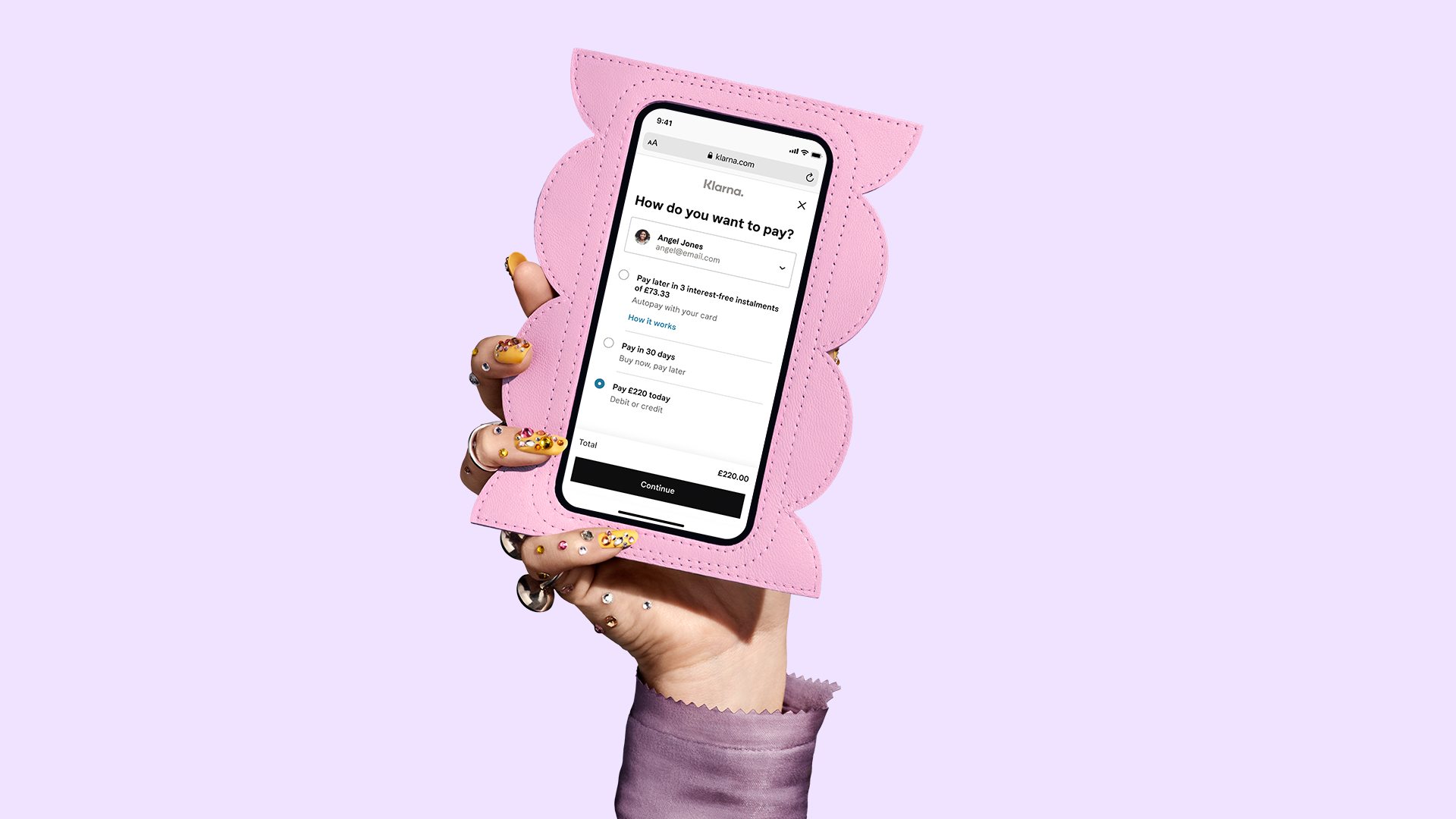

- With ‘Pay Now’ consumers in the UK can pay immediately and in full wherever Klarna is available.

- Part of a package of consumer-focussed changes to drive up standards across the UK payments industry.

- Even stronger credit and affordability checks, clear checkout language, simplified T&Cs, improved complaints handling and removal of last remaining late fees.

London - 18th October 2021 - Klarna, the leading global retail bank, payments and shopping service, today announces a package of changes to expand and strengthen its UK offering to give consumers more choice, clarity and control over how they pay. ‘Pay Now’ ensures UK consumers can always pay immediately and in full, wherever Klarna is available, with the same payment experience whether they choose to pay now or later. And in its continued drive to set standards for the UK payments industry, Klarna is also strengthening affordability checks and checkout language, providing more ways for consumers to challenge complaints decisions on the rare occasions this becomes necessary, and removing the last remaining late fees on its regulated financing product – all with immediate effect.

Putting consumers in control whether they pay now or pay later

While it is best known for Buy Now Pay Later (BNPL) in the UK, globally Klarna offers a wide range of payment and shopping services and its ‘Pay Now’ immediate payment option is extremely popular globally. Klarna’s UK payment and shopping options will now be consistent with those offered globally across 20 markets, giving consumers more choice, clarity and control over how they pay.

Pay Now is launched alongside a package of consumer-focussed changes to drive up standards across the UK consumer payments industry. Central to this, Klarna has begun to leverage its own well established Open Banking services, already connected to over 6,000 banks across 20 countries, to help support even better real-time lending decisions. In addition to the robust checks which Klarna performs on each and every purchase, consumers will be able to securely share income and spending data from their bank accounts to confirm they can afford future repayments. This supports Klarna’s commitment to financial inclusion by giving safe access to credit for those individuals with a limited conventional credit history, which is reliant on the use of traditional credit and does not reflect how people are choosing to make payments today. Klarna continues to drive innovation and change with the UK Credit Reference Agencies to enable all buy now pay later providers to share their data. When completed this work will reward the vast majority of Klarna customers who use BNPL responsibly with improved credit scores, and further protect consumers from accumulating debt.

As part of continuous efforts to lead the way on transparency and protection for consumers throughout their shopping and payment experience, Klarna has recently further strengthened the language visible at checkout to make it absolutely clear that BNPL options are credit products, with consequences for missed payments. It has also worked together with the consumer group, Fairer Finance, to make sure that terms & conditions are clear, simple and easy to understand. Additionally, Klarna has established its own complaints adjudicator for consumers who remain dissatisfied with how their complaint against Klarna has been handled. Klarna took this measure after being informed by the Financial Ombudsman Service (FOS) that complaints about BNPL products currently could not be referred to FOS on a voluntary jurisdiction basis. Up and running for over 6 months now, this service is providing valuable recourse for consumers on the rare occasions when they are not happy with the way a complaint has been handled.

Finally, Klarna has never charged late fees on its Pay in 30 or Pay in 3 BNPL products in the UK. From today, the company will now remove any remaining late fees from its regulated Financing product, which consumers use to spread the cost of higher value purchases over 6 - 36 months. This change drives better outcomes for consumers and means that, whatever Klarna product they choose to use, they can be confident they will not be charged late fees.

Sebastian Siemiatkowski, Klarna’s Co-founder and CEO said: “We firmly believe that most of the time, people should pay with the money they have, but there are certain times where credit makes sense. In those cases, our BNPL products offer a sustainable and no cost healthy form of credit - and a much needed alternative to high cost credit cards. The changes we are announcing today mean that consumers are fully in control of their payments whether they pay now or pay later.”

ENDS

Notes to editors:

How Klarna’s new checkout works

At an online checkout, customers will now see a single Klarna button presented alongside other payment methods accepted by the retailer. Consumers who select ‘Klarna’, will be able to choose either to pay immediately using a debit or credit card, or to pay in 30 days or over 3 instalments with no fees or interest. Klarna also offers longer-term, regulated Financing for larger purchases - this will be available with retailers that are authorised to offer it. Regardless of how they pay, consumers can keep track of their payments in the Klarna app.

For retailers, the single Klarna button streamlines the checkout and improves conversion.

Immediate payments will be rolled out at the majority of UK retailers by Q1 2022.

About Klarna

We make shopping smoooth. With Klarna consumers can buy now and pay later, so they can get what they love today. Klarna’s offering to consumers and retailers include payments, social shopping, and personal finances. Over 250,000 retail partners have enabled Klarna’s innovative shopping experience online and in-store. Klarna is one of the most highly valued private fintechs globally with a valuation of $45.6 billion. Klarna was founded in 2005, has over 4,000 employees and is active in 20 countries. For more information, visit klarna.com.

About Klarna Open Banking

Klarna’s Open Banking solution which today processes more than 200m transactions per year, and is connected to over 6,000 banks, offers third party providers simplified access to consumer bank account data via ‘Account information’ (AIS) and ‘Payment initiation’ (PIS) services in line with the Payment Services Directive (PSD2). The secure solution allows consumers, wishing to elevate the potential of their financial data, to better understand and engage with their finances in a more meaningful way.

About Fairer Finance

Fairer Finance is a ratings agency, consultancy and consumer group with a mission to create a fairer financial services market. It does this by campaigning, publishing product and customer experience ratings – and by working with companies who want its help and expertise to deliver better customer outcomes.

Contact

Dan Greaves