This week’s Congressional hearing on fintech will focus on a wide variety of topics, including Buy Now, Pay Later (BNPL). Healthy debate over BNPL should be encouraged and we support lawmakers and regulators working together to ensure consumers are protected. As lawmakers are discussing BNPL, we want to make sure they have the facts

about Klarna’s BNPL services offered in the US, especially compared to high cost credit cards.

How does Klarna’s BNPL service work?

At Klarna we have a product called Pay in 4 which is what is classified as a “BNPL” service. The product provides consumers with an interest-free alternative to credit cards. The the cost of each purchase is split into 4 payments spread over 6 weeks, with one payment at the outset and the remaining 3 payments collected every two weeks.

For us, it’s important that consumers are in control of their spending and stay on top of their payments, and unlike traditional credit cards, Klarna has a variety of features built into our products to ensure this is possible. So let’s take a look at what they are:

No revolving credit.

We do not offer ‘revolving’ credit – i.e. credit which can be postponed or ‘rolled over’ indefinitely. Our BNPL product comes with specific repayment schedules and we send multiple reminders to help our consumers stay on top of their payments. If a payment is missed, we pause the consumer’s account and restrict the use of our products until they are back on track in order to prevent debt accumulation.

Lending decisions on every transaction.

Using Klarna is not guaranteed and we don’t provide an open line of credit like predatory credit cards. We check a customer’s ability to pay each and every time someone wants to make a purchase and we make a new underwriting decision for every transaction, releasing a small amount of credit linked to a specific purchase.

Clear repayment schedules.

Every time a consumer makes a purchase, we display at the checkout, a payment schedule which is clearly laid out so consumers know when they will be charged, and how much.

Payment reminders and budgeting tools.

To keep people on track, we send additional emails and in-app reminders so consumers are always on top of what’s still to come, what their current balance is and their future payment schedule. We also offer budgeting tools in the Klarna app.

Fast facts about Klarna’s Pay in 4:

NO interest charges

NO ability to revolve

Real time underwriting for each and every transaction

NO compounding interest

NO annual fees

Restriction of services after a missed payments to prevent debt from building up

Capped late fees

Clear and relevant disclosures

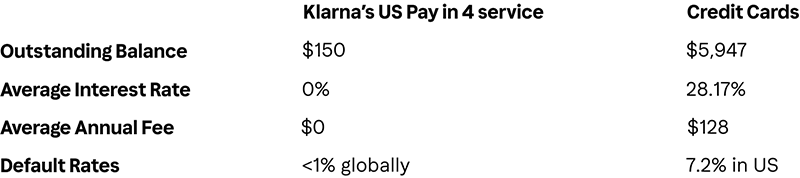

So how does Klarna’s BNPL service compare to credit cards?

Americans are drowning in debt. With high-inflation, higher interest rates, the depletion of pandemic savings, not to mention the resumption in student loan repayments, credit card balances have surpassed

for the first time ever! While credit has a role in society – the business model at the heart of banking is broken and is designed to keep people in perpetual debt. At Klarna, we’re offering a designed to keep people out of debt and access credit in a more sustainable manner.A big difference between Klarna and credit card companies comes down to our business model, which is based on adding value to the shopping and payments experience for both consumers and retailers. Our products are not designed to get people to borrow as much as possible, at the highest possible rate. Unlike credit cards who make their money when people miss a payment, our business model relies on people paying us back on time and in full – so our intent is that people spend responsibly. ‘Let’s take a quick look at the facts:

Unlike credit card companies who make money when consumers fall behind in payments, the vast majority of our revenue globally comes from retailers by providing them with smoooth payment services, reduced financial risk through our interest-free Pay Later products, and increasingly tailored marketing support that helps them connect with consumers.

Is Klarna Regulated?

We are a fully licensed bank in the EU, and Klarna is very comfortable operating in a regulated environment and wholeheartedly supports the regulation of the BNPL sector. In the US, Klarna is subject to stringent federal and state oversight, complying with numerous regulations that drive trust and transparency with both regulators and customers, including:

Extension of Credit (Regulation B)

Electronic Funds Transfers (Regulation E)

Unfair and deceptive acts and practices (Regulation V, “UDAAP”)

Anti-money-laundering laws and regulations; and

Explanation of information-sharing practices and safeguarding of sensitive data (Gramm-Leach-Bliley Act).

We support regulation that is proportionate to the risk BNPL poses to consumers. As the data clearly shows, and outlined in the graph above, BNPL does not pose the same risk to consumers. Low-cost, low-risk, no-interest products like BNPL should not fundamentally be regulated in the same fashion as high-cost credit products which rely on consumer fees and revolving debt. We support appropriate guardrails that protect consumers, not banks, while still allowing for innovation, competition and alternatives to high cost credit.

Let’s Work Together

We are thankful to lawmakers for making space for a conversation on BNPL and the larger fintech ecosystem, and we look forward to continuing to work together to create a better world for consumers.

If you’d like to hear more, don’t forget to follow us on

.