There’s been a lot of talk around the buy now pay later sector over the past few months. We get it, it’s a relatively new industry which is disrupting the traditional consumer credit space and becoming increasingly popular – hello 14 million UK Klarna customers! As the market leader, we wanted to bring some more clarity on this booming sector. That’s why we recently published the independent report ‘

’. Curious to know more? Here are 10 stats from the report that might surprise you!

1) BNPL accounted for 3.6% of all online retail sales in the UK in 2020.

There’s no doubt that the BNPL sector is growing at a very fast pace, especially as payment preferences are changing and many are embracing modern and flexible payment methods which better suit their needs.

2) £4.1bn spent in 2020 using BNPL.

While this sounds like a big number, it’s still relatively small compared to the credit card market. The total amount spent on credit cards, which are declining in popularity, in the twelve months to October 2020 was £155bn.

3) BNPL saved consumers £76m in interest fees last year.

If all BNPL purchases had been made on credit cards instead, it could have cost consumers £76m in interest charges, let alone late fees, fines or membership costs. As BNPL continues to grow, so will the cost savings for consumers!

4) BNPL helps people manage their finances.

Consumers love BNPL not only because it’s a flexible and convenient way to pay. 64% of those who have used a BNPL service thought that the flexibility offered helped them manage their finances. What’s more, when respondents were able to identify a specific provider, the rate of those who said BNPL helped them with money management spiked to 80%.

5) 10.4 million consumers used BNPL in the past year.

Around a fifth of the UK’s adult population used BNPL in 2020 while 17 million have used it at some point in their lives.

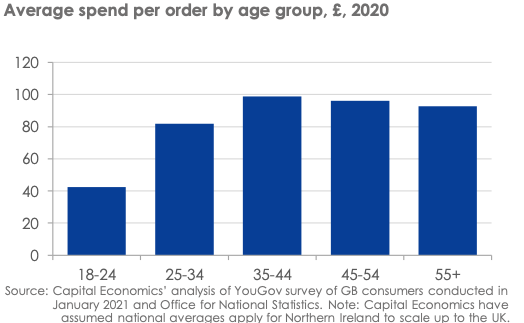

6) Younger generations spend less on average.

That’s right. We’ve heard a lot – probably too much – about how young people are irresponsible with their finances. Well, we like to stick to the data. And data show that in 2020 the average BNPL order value for those between 18-24 was £42, which is about half of that of all other age groups.

7) Electronics and tech products are the most popular with BNPL.

While shoppers enjoy using BNPL for a variety of goods, electronics and tech products have been the most popular purchases since the start of the pandemic. Over 30% of consumers that used BNPL in the past year bought an electronic or tech item that they would not have otherwise purchased. This may reflect how spending habits have changed during the pandemic and our increased reliance on technology for both work and leisure.

8) BNPL provides extra reassurance when consumers try new retailers.

It can be a bit daunting when you’re shopping online but haven’t used a retailer before, so trusting your payment provider can make a huge difference. 78% of UK consumers that have used BNPL services said that the security it provides when buying from unknown sellers was important to them.

9) Credit cards are the most common alternative to BNPL.

If BNPL had not been available at the checkout, a third of the purchases would have been made with another and potentially more expensive form of credit. 70% would have used a credit card, over 20% would have used an overdraft, 12% would have used a bank loan and 5% said that they would have used payday loans. When you think that the average APR for a credit card is over 20% and overdrafts, bank loans and pay day loans are even higher, that’s a lot of interest customers could end up paying.

10) Consumers value flexible return policies.

With non-essential stores closed during the pandemic, shoppers had to rely on online shopping for their purchases. However, it’s hard to understand how a particular item really is – or fits – when you can only see it through a computer screen. That’s why many use BNPL, with 78% of users saying that flexible returns were important in their decision to use BNPL in their online purchases.

If you want to learn more about buy now pay later check out the

.